Compound Interest is also called “Interest On Interest”. The interest for the first period (year) is added to the principal at the end of the year and starts earning interest for the new amount in the next year.

e.g. If you have invested $ 100 in a Bank Fixed Deposit at 5% interest, then at the end of the first year, the interest will be $5.00.

The principal for the next period will be = Original Principal + First year interest = 100 + 5 = $105.00

In the 2nd year, the 5% interest will be applied to the new principal $105. So interest for the 2nd year will be = 105 * 0.05 = $ 5.25.

Note that the interest in the second year is higher than the interest in the first year. This is called the power of compounding. As the investment period grows, the effect will be more. There will be a time when the interest component will be more than your contributions. To see the effect, click on Display Monthly Breakup. The compounding effect meaning is popular and applied in our compound interest calculator.

The Rule of 72 is a quick method to estimate how long it will take for a particular amount of money to double with an annual interest rate. Any investment with a fixed rate and compound interest within a reasonable range is eligible for use. To find the number of years it will take to double, divide 72 by the annual rate of return.

E.g. it will take about nine (72 / 8) years for $100 with a fixed rate of return of 8% to grow to $200. Remember that an “8” represents 8%, so users should not convert it to decimal. Therefore, one would use “8” rather than “0.08”.

Rule of 72 also works on the same method of compounding that our compound interest calculator uses. Additionally, be mindful that the Rule of 72 is an approximation, not exact.

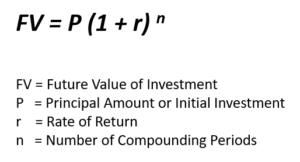

If a person deposits $1000.00 at the beginning of the year @5% annual interest rate, then at the end of 2 years,

P = 1000 r = 0.05 (= 5% or 5/100) n = 2 years

Then, by applying the above formula, the maturity amount will be –

(1+0.05)^2 = $1102.5

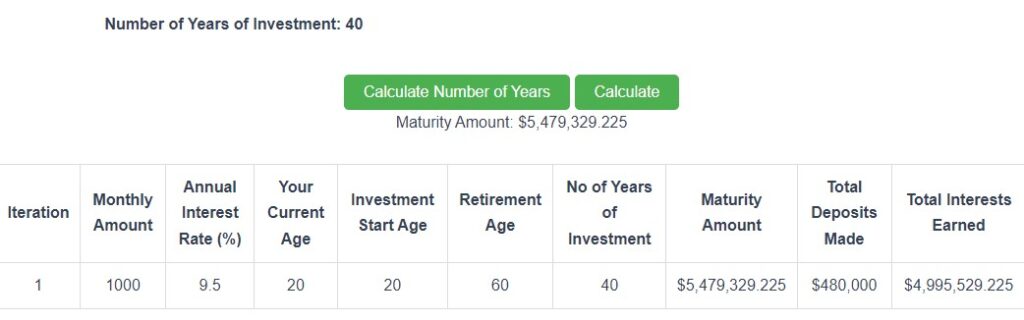

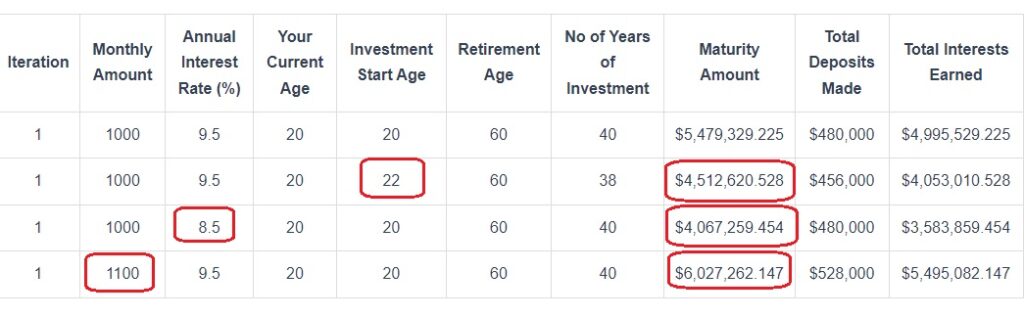

In a single browser session, one can compare the five results to determine the savings amount, number of years, and expected annual return on investments for a desired sum at retirement.

The three ways to harness the power of compounding for a better future are –

- Start your investment early – You can see from the sample results from the compound interest calculator that, by reducing the investment period by just two years, the person is losing close to a million USD in maturity value. Always allow as much time as possible for your investment to grow.

- Invest as much as possible – The more you invest, the more you will get. As you can see, by increasing the monthly savings amount by just $100, the retirement kitty becomes fatter by nearly $500 K.

- Earn return as much as possible – Your investments should return as much as possible. In the same example, you can see, a reduction in interest rate by 1%, removes close to $ 1.5 million from the retirement kitty.

For more details, refer to our Blog here.